View / Download January 2021 Article – PDF File

Tax Trends and Developments Column – Michigan Family Law Journal

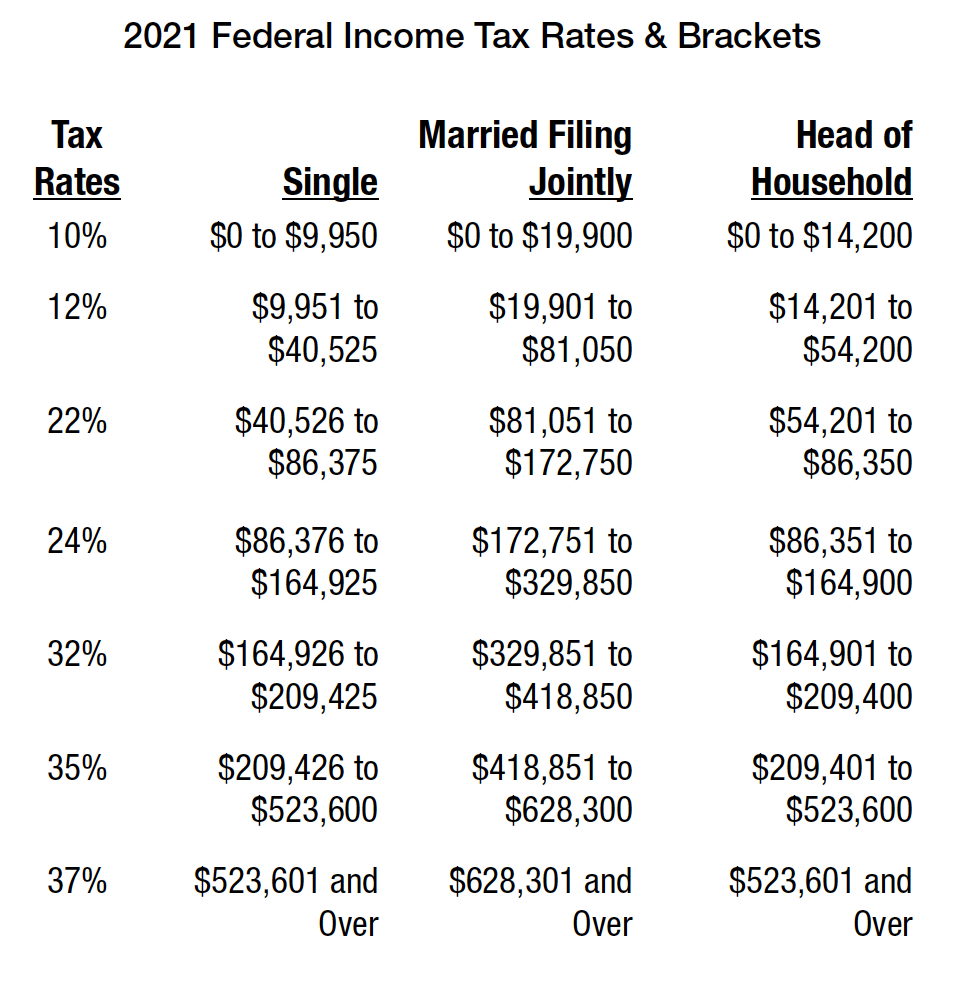

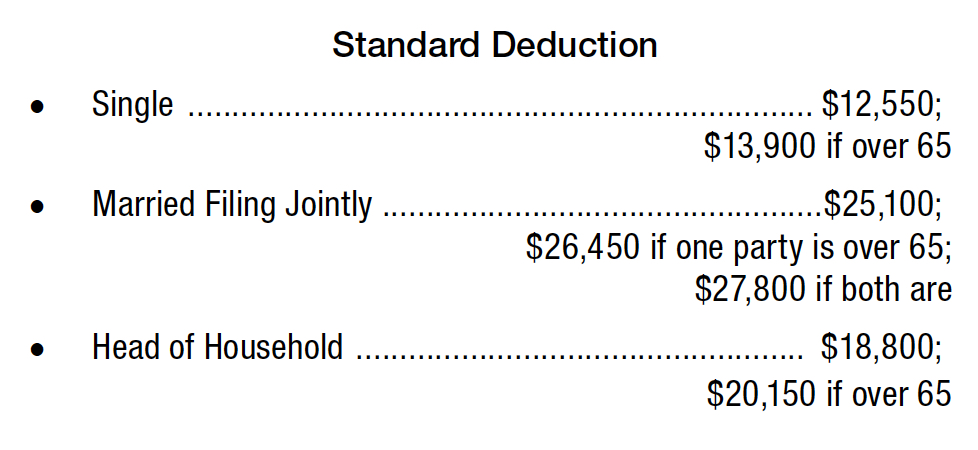

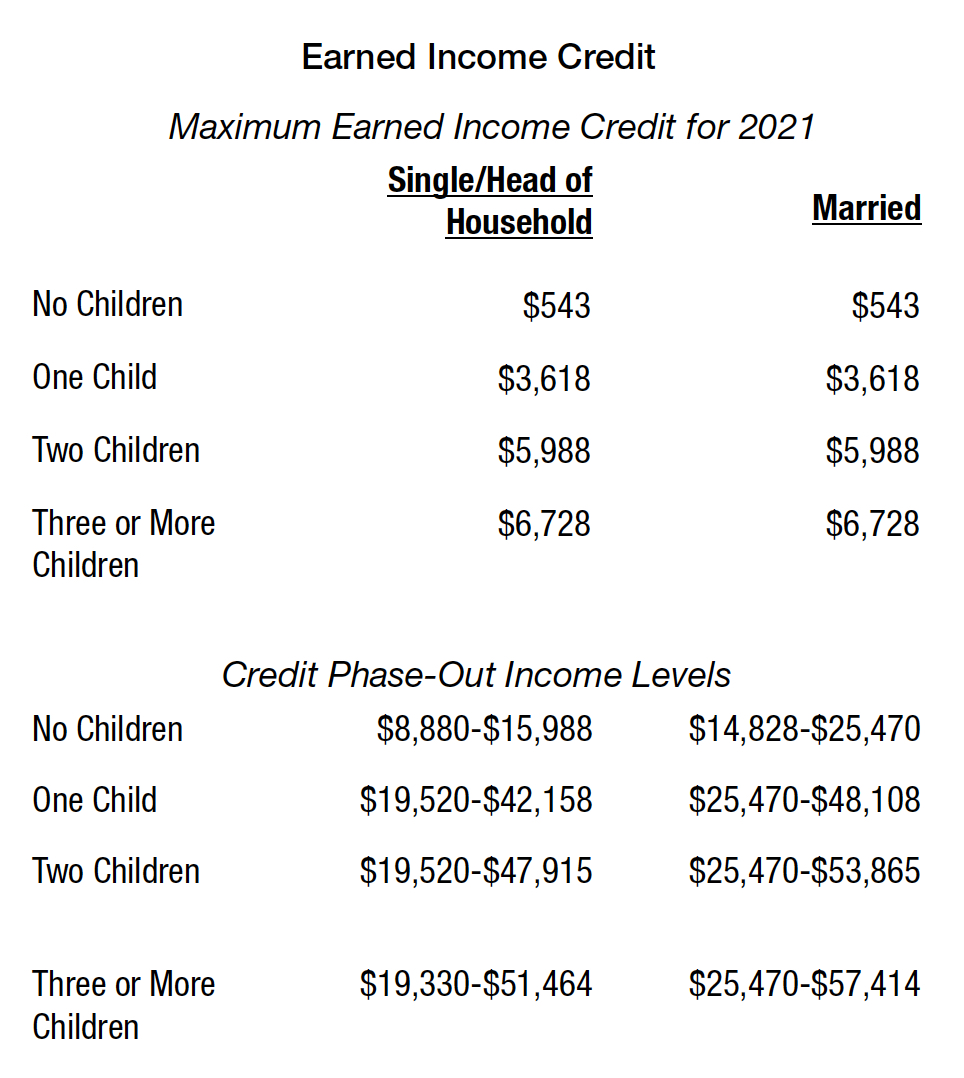

Federal Income Tax

The following are inflation adjusted tax rates and standard deductions for 2021 as announced by the IRS (IR-2020-245).

Personal Exemption

There is no personal exemption. It was eliminated by the Tax Cuts & Jobs Act. of 2018.

2021 Long-Term Capital Gain Rates

- 0% for taxpayers in the 10% or 12% brackets.

- 15% for:

- Single filers with taxable income between $40,400 and $445,850

- Married Filing Jointly with taxable income between $80,800 and $501,600

- Head of Household with taxable income between $54,100 and $473,750

- 20% for taxpayers with taxable incomes exceeding the high end of the above ranges

Child Tax Credit

The Child Tax Credit is $2,000 for qualifying children.

A qualifying child is, in general, a child of the taxpayer who resides with the taxpayer for more than half of the year.

Michigan Income Tax

Tax Rate

The Michigan income tax rate remains unchanged at a 4.25% flat rate.

Personal Exemption

The number of personal exemptions a Michigan taxpayer could claim had previously been tied to the number claimed for federal tax purposes. With the elimination of federal tax personal exemptions, Michigan enacted Senate Bill 748 (Bill), signed by Governor Snyder on February 28, 2018.

Under the Bill, the reference to federal exemptions is removed. The Michigan personal exemption deduction for 2021 is $4,900.

About the Author

Joe Cunningham has over 25 years of experience specializing in financial and tax aspects of divorce, including business valuation, valuing and dividing retirement benefits, and developing settlement proposals. He has lectured extensively for ICLE, the Family Law Section, and the MACPA. Joe is also the author of numerous journal articles and chapters in family law treatises. His office is in Troy, though his practice is statewide.

View / Download January 2021 Article – PDF File

Complete Michigan Family Law Journal available at: Michigan Bar website – Family Law Section (subscription required)