View / Download Aug/Sept 2022 Article – PDF File

Tax Trends and Developments Column – Michigan Family Law Journal

Estimated tax payments made – and/or taxes withheld – during the year of divorce may be a marital asset. Tax refunds or, overpayments applied to next year’s tax, attributable to tax payments made during marriage may also be a marital asset.

And, it may cut the other way – that is, estimated tax payments and/or taxes withheld may be less than the actual tax on marital income received and shared during the year of divorce.

In this regard, note the following:

- Separate Returns for Year of Divorce – Whether divorcing parties can file a joint return or must file separate returns depends on their marital status as of December 31. If divorced as of that date, they must file separate returns for their respective separate incomes and deductions.

- Estimated Payments Automatically Are Credited to the Husband – Since the husband’s social security number (SSN) is generally listed first on joint estimated payment vouchers (Form 1040ES) made during marriage, such payments will automatically be credited to him unless there is a written alternative provision agreed on by the parties.

- The same applies to tax overpayments on the parties’ last joint return applied to the following year’s tax.

- Estimated Tax Payments and Tax Withheld During Marriage Are Marital Funds – Absent unusual circumstances, estimated tax payments and tax withheld during marriage are made with marital money – essentially half by each party.

The above matters are often not addressed in divorce settlements. The following presents (1) observations on such tax payments and (2) applicable tax law.

Tax Payments Made During the Year of Divorce

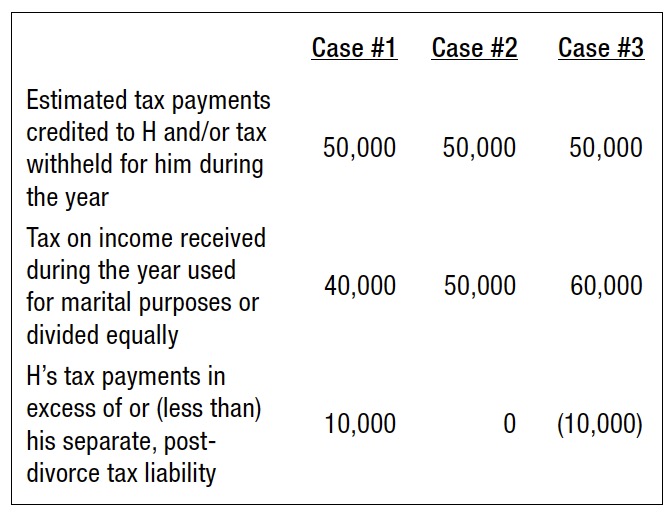

Example – Assume the following alternative facts for joint estimated tax payments made by – and/or withheld on behalf of H – during the year of a divorce for which the judgment is entered on December 30.

So, in Case #1, H will receive a windfall unless W’s attorney identifies the overpayment and makes an offsetting adjustment. Half of H’s $10,000 overpayment was made with W’s share of marital funds.

In Case #3, it is H’s attorney who needs to (1) identify that H will pay $10,000 of his own funds on income equally shared with W and (2) make an offsetting adjustment. When paying the $10,000, H will, in effect, be paying both his and W’s $5,000 shares of the tax on marital income.

Agreement to Apportion Joint Estimated Tax payments – IRS Publication 504 – “Divorced or Separated Individuals” – provides that divorced parties may agree on the division of joint estimated tax payments made during marriage.

Because the IRS credits the account of the spouse who’s SSN appears first on the estimated tax voucher (Form 1040ES) – almost always the husband’s – if the other spouse (assume W) claims any of the joint estimated tax payments on a separate return, W should indicate the ex-spouse’s SSN on page one of her IRS Form 1040 in the designated space. If W has remarried, she should enter the current spouse’s SSN in the appropriate space and enter the ex-spouse’s SSN, followed by “DIV,” on the line at the bottom of page one, where estimated tax payment credits are claimed.

Tax Refunds and Overpayments Applied to Next Year’s Tax

It is common practice to provide for the division of tax refunds resulting from the parties’ final joint income tax return. But, in some cases, parties filing a joint return will apply all or a part of any tax overpayment to the following year’s tax rather than having it refunded. This frequently occurs when a return is on extension and filed after April 15 and the prior year overpayment is needed to cover current year tax to avoid the underpayment penalty.

The IRS has ruled that it will abide by an agreement of spouses who are no longer married regarding the apportionment of an overpayment of tax on a prior year’s joint income tax return that the parties elected to apply to the following year’s tax liability. Rev Rul 76-140.

However, here, too, because the IRS credits the account of the spouse whose SSN appears first on the tax return, if the other spouse claims any of the applied overpayment, the other spouse should indicate the ex-spouse’s SSN on page one of his or her IRS Form 1040 in the designated space. If the other spouse has remarried, he or she should enter the current spouse’s SSN in the appropriate space and enter the exspouse’s SSN, followed by “DIV,” on the line at the bottom of page one, where estimated tax payment credits are claimed.

Practice Pointers

- Discover Tax Situation – As part of discovery, the tax overpayment or underpayment status of the parties should be determined. This can often be provided by the parties’ tax preparer.

- Over Withholding – The owner of a closely-held business can arrange excessive tax withholding. If undetected, the money that should be in marital accounts to divide will instead accrue 100% to the owner as a tax refund. The excessive withholding can be done on the last day of the year. So, the fact that withholding was not excessive on a September 30 pay stub is not a reliable safeguard against withholding manipulation.

- Rather, the owner’s W-2 should be reviewed for the relationship between (1) income and (2) income tax withheld to discover whether there is excessive withholding.

- Specific Divorce Settlement Provisions – In addition to discovering the parties’ “tax situation,” the settlement agreement should include express provisions regarding matters such as division of refunds, splitting joint estimated tax on separate returns, and ensuring an equitable sharing of tax on marital income for the year of divorce.

IRS Publication 504 – “Divorced or Separated Individuals”

This an excellent 30 page summary of divorce taxation. It covers the following topics:

- Filing Status

- Exemptions

- Alimony

- QDROs & IRAs

- Property Settlements

- Tax Withholding and Estimated Tax

Publication 504 was updated in October 2021 and has a 2 page detailed index.

It is available for download at http://www.irs.gov/pub/irspdf/p504.pdf

About the Author

Joe Cunningham has over 25 years of experience specializing in financial and tax aspects of divorce, including business valuation, valuing and dividing retirement benefits, and developing settlement proposals. He has lectured extensively for ICLE, the Family Law Section, and the MACPA. Joe is also the author of numerous journal articles and chapters in family law treatises. His office is in Troy, though his practice is statewide.

View / Download Aug/Sept 2022 Article – PDF File

Complete Michigan Family Law Journal available at: Michigan Bar website – Family Law Section (subscription required)

Read More “Aug/Sep 2022 : Estimated Tax Payments; Tax Refunds & Overpayments”